Crypto Cashouts & UAE Banks: Avoiding Account Freezes

The Middle Eastern Banking Perimeter: Structural Shifts in 2026

Moving high-stakes capital from digital assets into traditional UAE bank accounts requires navigating strict Central Bank monitoring systems. Unstructured transfers from crypto sources can trigger automated compliance blocks, leading to immediate account freezes under current anti-money laundering frameworks.

The regulatory environment for digital asset settlement in the Middle East has entered a highly sophisticated phase. Following the formal integration of Federal Decree-Law No. 25/2025, the General Commercial Gaming Regulatory Authority (GCGRA) has fully formalized the pathways for commercial gaming wealth. At the same time, the Central Bank of the UAE (CBUAE) has tightened its compliance requirements for Licensed Financial Institutions (LFIs). This shift impacts how banks handle inbound fiat liquidity originating from decentralized sources. The days of casual, unmonitored peer-to-peer transfers are over.

CBUAE Anti-Money Laundering Architecture

VARA/ADGM Certified Nodes

- Automated KYC/AML Check

- Straight-Through Processing

- Clear Audit Trail Created

Unverified P2P / Mixers Nodes

- Immediate Transaction Pause

- Suspicious Activity Report (SAR)

- Risk of Full Account Freeze

The launch of major brick-and-mortar gaming projects like the $5.1 billion Wynn Al Marjan Island resort in Ras Al Khaimah is drawing massive international capital to the region. This influx of high-stakes players has increased the volume of large fiat-to-crypto settlements. Consequently, local banks have deployed advanced artificial intelligence monitoring systems. If a user routes massive profits from a digital platform directly into a standard savings account without a verified audit trail, internal algorithms instantly flag the transfer as a high-risk event. This tension defines the modern market. Players need to move capital efficiently, but traditional banking systems are built to prioritize absolute compliance over speed.

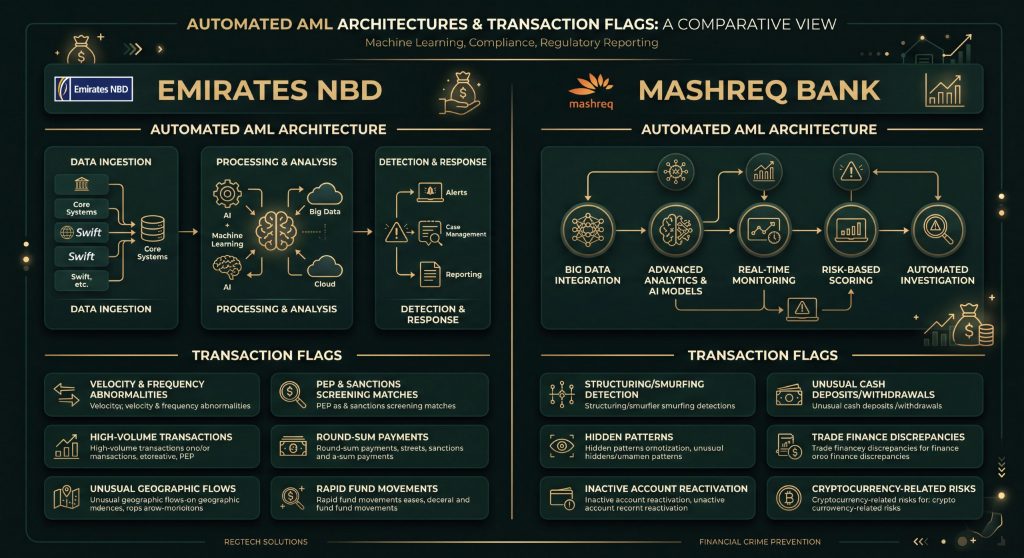

Emirates NBD and Mashreq: Automated AML Architectures and Transaction Flags

Emirates NBD and Mashreq utilize automated compliance engines that track the exact origin, velocity, and counterparties of all incoming transactions. Transfers from unverified accounts or high-risk crypto platforms will immediately trigger internal compliance reviews.

Emirates NBD and Mashreq handle digital asset transactions using fundamentally different operational approaches. Emirates NBD has adopted a regulated, institutional approach to digital assets. The bank has integrated closed-loop crypto custody within its Liv X digital banking app through partnerships with Aquanow and Zodia Custody. This system allows users to trade five major cryptocurrencies safely. However, it functions as a closed loop, meaning external wallet withdrawals are completely restricted. For larger transactions, Emirates NBD permits fiat transfers to and from platforms licensed by the Virtual Assets Regulatory Authority (VARA) or the ADGM’s FSRA. The system runs smoothly as long as you use authorized, compliant endpoints.

VARA-Licensed Exchange

Straight-Through Fiat Transfer

High-Velocity Cash Flows

AI Pattern Analysis

Mashreq Bank focuses heavily on data analytics and automated pattern recognition across its Mashreq Neo and NeoBiz platforms. This reliance on automated compliance systems can create challenges for high-volume players. Mashreq’s AI algorithms monitor incoming cash flows for specific risk indicators, including:

- Rapid velocity spikes: Multiple consecutive inbound transfers under AED 50,000 executed in compressed timeframes.

- Counterparty contamination: Funds originating from or routed through corporate entities linked to unverified OTC trading.

- Mismatched transaction profiles: Sudden seven-figure inflows into an account architecture that historically handles standard retail or employment volume.

When an automated flag is triggered, the architecture instantly pauses the transaction and generates a Suspicious Transaction Report (STR). This automated protocol freezes the capital asset until a tier-1 compliance officer manually reviews and clears the original source of wealth.

The P2P and OTC Off-Ramping Matrix: Mitigating Third-Party Contamination

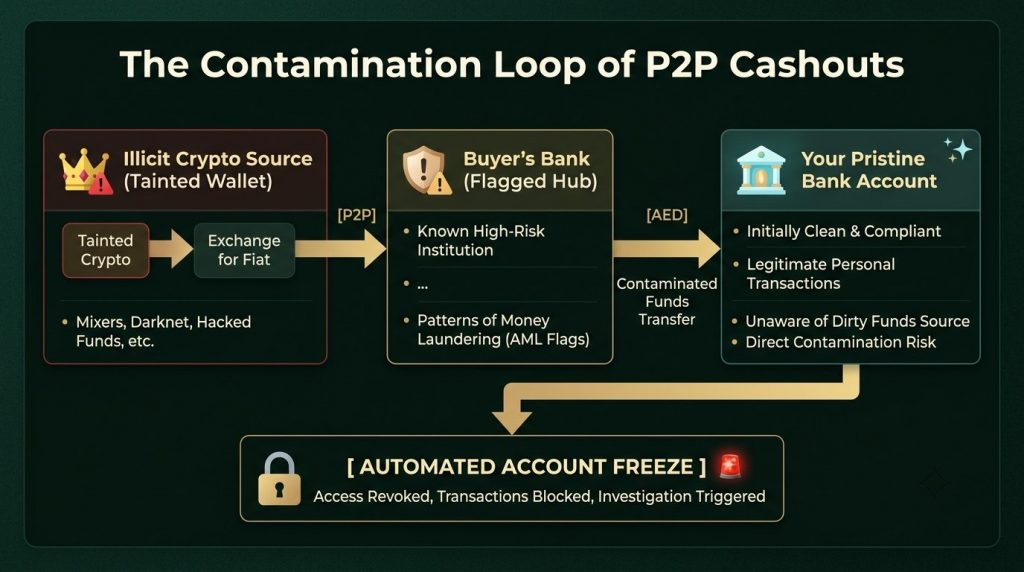

Direct Answer: Peer-to-peer (P2P) marketplaces carry a high risk of account freezes due to the potential for third-party fund contamination. High-stakes players protect their banking relationships by using VARA-licensed Over-The-Counter (OTC) desks for all large liquidations.

Using standard P2P directories on global crypto exchanges is a risky strategy for liquidating large volumes of casino capital in the UAE. The primary risk is third-party bank account contamination. When you sell stablecoins via a P2P directory, you are relying on a random buyer to transfer fiat currency to your bank account. You have no control over the history of those funds. If that buyer previously interacted with an illicit wallet, an unverified platform, or a fraudulent scheme, their bank account becomes flagged. The moment they transfer funds to you, that negative compliance rating spreads to your account. Emirates NBD or Mashreq will immediately freeze your entire balance as part of an ongoing investigation.

Standard P2P Marketplaces

Random Counterparties: Capital origin is completely unverified, exposing your bank account to illicit retail velocity loops.

Contamination Spread: Flagged buyer credentials instantly pass negative corporate compliance ratings to your clean assets.

Sanction Vectors: Extreme vulnerability to automated AML triggers at Emirates NBD or Mashreq Bank, resulting in immediate profile lockouts.

Licensed Corporate OTC Desks

Institutional Liquidity: Capital originates directly from licensed corporate treasury accounts with fully audited asset records.

Pre-Vetted Flow: All inbound transactions pass automated cryptographic KYT (Know-Your-Transaction) tools prior to routing.

Banking Immunity: Transparent legal origin ensures straight-through processing without generating suspicious pattern reports.

For high-volume players, VARA-licensed OTC desks offer a much safer alternative. These institutional desks act as direct liquidity counterparties, ensuring a secure and transparent transaction path. Typical trading spreads for large digital asset blocks run between 0.5% and 1.5%, depending on liquidity conditions. This fee is a reasonable cost to pay for security. The OTC desk accepts your digital assets, verifies their on-chain history using advanced forensic tools like Chainalysis, and issues a clean fiat transfer from their corporate bank account. This transaction includes a clear, compliant description code. This documentation provides a transparent audit trail, allowing your bank’s compliance team to process the inflow safely without triggering fraud alerts.

Decentralized Liquidity Pools and Stablecoin Routing Protocols

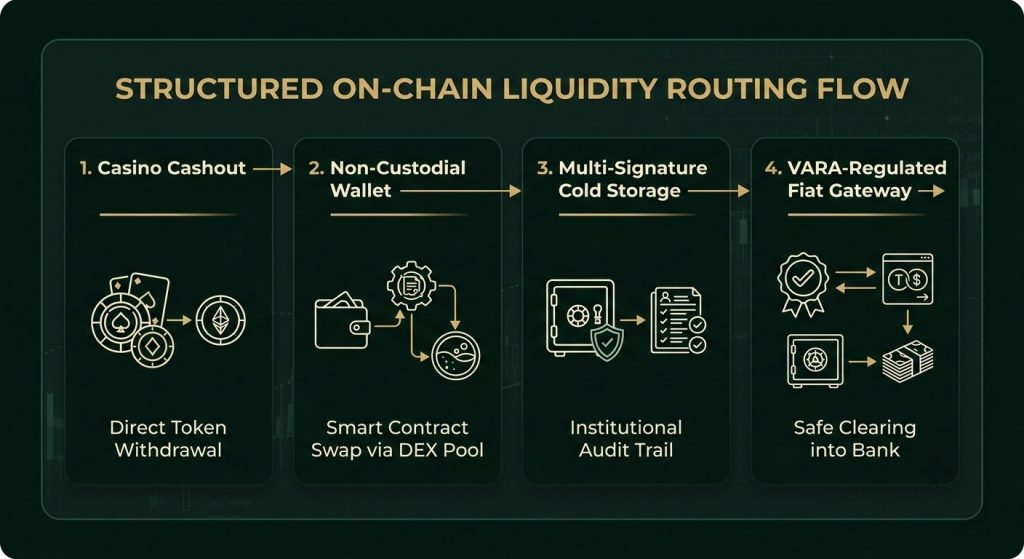

Direct Answer: High-stakes players use non-custodial decentralized liquidity pools and multi-signature intermediate wallets to clean their transaction histories before moving capital to regulated gateways. This structural layer prevents gaming platforms from interacting directly with personal bank accounts.

Smart portfolio management requires separating your gaming activity from your core banking relationships. If you cash out directly from an international platform to an account linked to a Dubai Casino portal, you expose your entire financial footprint to bank scrutiny. Sophisticated webmasters avoid this direct exposure by utilizing decentralized routing protocols. The process begins on-chain by routing profits through highly liquid decentralized protocols, such as Uniswap or Curve Finance. This routing mixes the assets with institutional capital, effectively breaking the direct link to the original gaming transaction.

Once the tokens are swapped into regulated stablecoins, the capital is moved to an intermediate non-custodial multi-signature wallet. This wallet acts as a private clearinghouse. The assets are stored here until the user initiates a withdrawal through a regulated local fiat gateway. In June 2026, Binance Dubai launched direct AED bank rails with a fixed 10 AED withdrawal fee. This service gives players a secure, licensed method to off-ramp capital into local bank accounts. By utilizing a regulated intermediary exchange, you present your local bank with an audit trail from a licensed domestic entity rather than an offshore platform.

Comparative Playbook: Managing Cashouts for High-Stakes Capital

The table below outlines the structural trade-offs of the primary off-ramping methods available to players managing high-stakes capital within the UAE financial ecosystem.

| Cashout Methodology | Execution Risk Profile | Settlement Speed | Compliance Documentation Strength | Optimal Transaction Scale |

| Direct Offshore Bank Wire | Extremely High: High probability of an immediate account freeze and manual AML review. | 3 to 5 Banking Days | Very Weak: Triggers red flags due to lack of a verified regional audit trail. | Not recommended for any volume. |

| Standard P2P Exchange Directory | High: Risk of account freeze due to counterparty account contamination. | 10 to 30 Minutes | Weak: Transactions appear as random transfers from unverified third-party accounts. | Under AED 15,000 for minor liquidations. |

| VARA-Regulated Exchange Rails | Minimal: Secure, compliant routing through recognized domestic banking channels. | Same-Day Settlement | Excellent: Supported by local exchange statements and fixed fee records. | AED 15,000 to AED 500,000. |

| Licensed Institutional OTC Desk | Negligible: Full institutional compliance checks with direct bank clearing. | 1 to 2 Hours | Flawless: Provides custom contract declarations and forensic on-chain validation. | Over AED 500,000 for institutional-grade wealth. |

Choosing the appropriate off-ramping method depends on the scale of your transaction. For regular, moderate volume, using localized, regulated exchange accounts is efficient. However, when managing significant capital, moving funds requires the specialized support of an institutional OTC desk to protect your banking assets.

Operational Verification: Preparing the Source of Funds Audit Trail

Direct Answer: Safely resolving an automated banking block requires presenting a clear, documented audit trail that shows every step of your funds’ movement from the original platform to your wallet. You must provide clear documentation before your bank’s compliance team requests it.

If your account at Emirates NBD or Mashreq is flagged for review, the resolution speed depends entirely on the quality of your documentation. You must prove the absolute legitimacy of your capital. Do not rely on verbal explanations or generic screenshots. A professional source-of-funds package must be compiled cleanly and systematically.

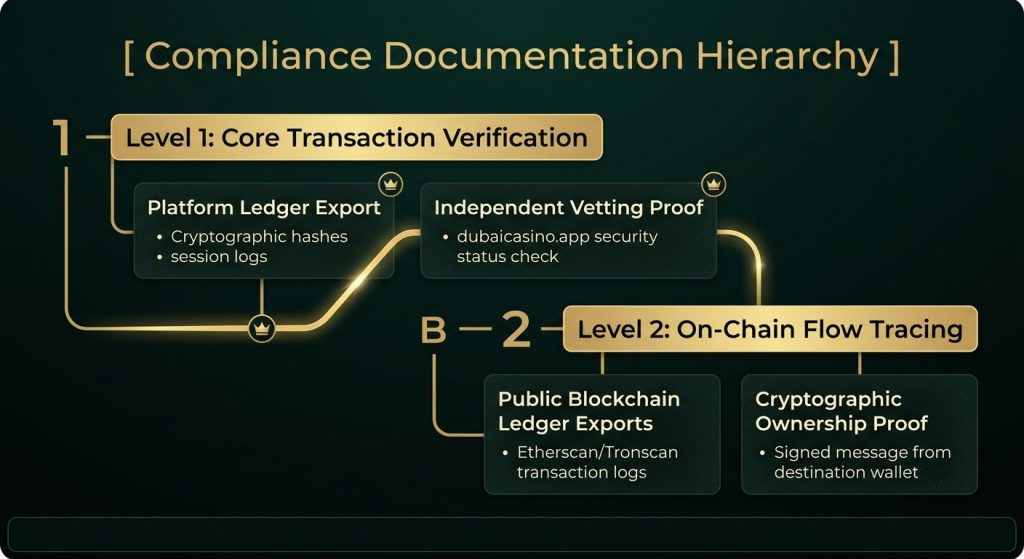

Your documentation package must contain two distinct verification layers:

1. Core Transaction Verification

- Platform Ledger Exports: Download the full history of your transactions from the source platform, including cryptographic transaction hashes, exact timestamps, and full account details.

- Independent Security Verification: Include proof that the underlying platform has been vetted for security. Our teams use data from independent screening platforms like dubaicasino.app to confirm the legitimacy of the source venue. This step proves to compliance officers that your funds did not originate from a high-risk or predatory offshore site.

2. On-Chain Flow Tracing

- Public Blockchain Ledger Exports: Provide clear tracking sheets from public block explorers (such as Etherscan or Tronscan) that illustrate the complete flow of tokens through your intermediate routing wallets.

- Cryptographic Ownership Verification: Be prepared to provide a signed message from your private non-custodial wallet to prove you control the underlying addresses.

When this completed package is submitted alongside your local transaction receipts, it answers all typical compliance questions regarding wealth creation and transmission asset agility.

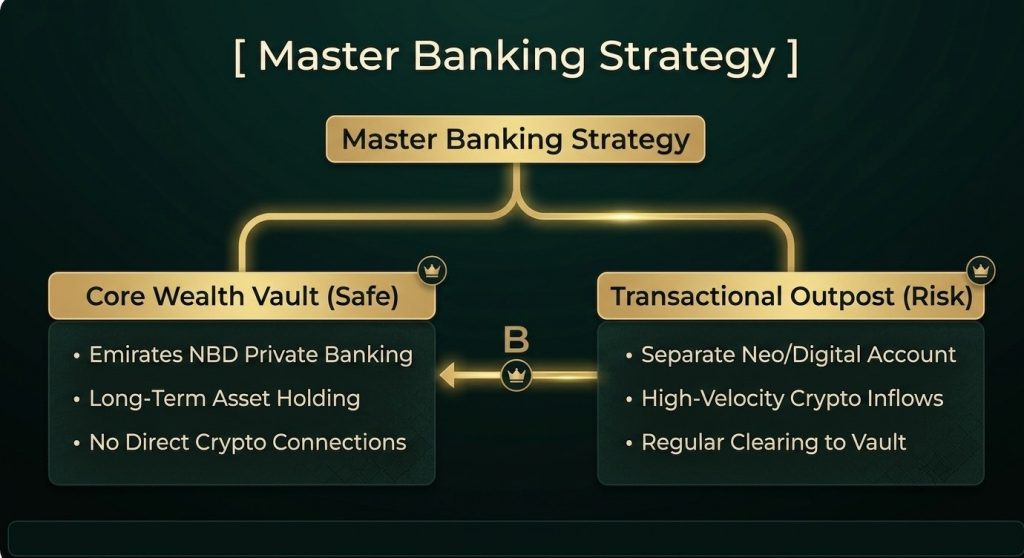

Defensive Banking Practices for High-Volume Digital Exploits

Direct Answer: Protecting your primary financial assets requires maintaining dedicated transactional accounts that are completely separate from your core corporate or savings banking relationships. This isolation ensures that a compliance dispute on one account will not freeze your entire financial infrastructure.

Do not run high-velocity digital asset cashouts through the same bank account you use to pay your corporate rent, manage salaries, or hold long-term investments. That is an operational mistake. High-volume players apply a strict rule of structural isolation: they open a dedicated transactional account solely for processing inflows from digital asset exchanges.

This strategy is highly effective. If an automated algorithm at Mashreq or a similar digital banking app triggers a sudden freeze on your transactional outpost, your primary wealth vault remains safe and unaffected. You retain full liquidity to cover your ongoing living costs and corporate obligations. While your compliance team works to resolve the flag on the transactional account, your daily life continues without disruption. This structure manages risk effectively, ensuring that compliance hurdles do not create a personal financial crisis.

The Strategic Balance of Modern Wealth Migration

Direct Answer: Navigating the modern UAE financial ecosystem requires combining the convenience of digital gaming with institutional banking compliance. Utilizing verified routing structures and independent screening platforms is the only way to manage high-stakes capital safely.

The transformation of the Middle Eastern gaming market is creating incredible opportunities for international players. Landmark physical developments like Wynn Al Marjan Island are establishing the region as a premier global hub for luxury entertainment, while advanced digital platforms offer unmatched privacy and efficiency. However, accessing this ecosystem safely requires strict operational discipline. The compliance tools deployed by major regional banks are designed to identify and block unstructured, anonymous wealth transfers.

To succeed in this environment, you must build your financial routing strategies around transparency and data verification. Avoid high-risk P2P networks, use authorized domestic exchanges, and pre-assemble clear transaction audit trails. Utilizing independent validation platforms like dubaicasino.app allows you to select safe gaming environments while gathering the compliance data necessary to satisfy bank audits. By managing your cashouts with the same discipline you use for game strategy, you protect your capital and ensure long-term financial security in the region’s rapidly growing market.